Getting Started

All steps outlined in the following are provided in the template for R packages using lesstimate. The C++ code can be found in the src directory of the package.

All steps outlined in the following are provided in the template for C++ packages using lesstimate. The C++ code can be found in the linear_regression.cpp file of the package.

lesstimate was initially a sub-folder of the lessSEM package. Therefore,

the default is currently to still assume that you are using the library in an R package.

In the common_headers.h-file,

you will find a variable called USE_R. If this variable is set to 1 (default), lesstimate

is setup to be used from R. If USE_R is set to zero, the library no longer relies on the R packages

Rcpp (Eddelbuettel et al., 2011) or RcppArmadillo (Eddelbuettel et al., 2014). The library can now be used in

C++ projects as long as the armadillo (Sanderson et al., 2016)

library is installed.

Interfacing to lesstimate

As outlined in the introduction, the optimizers in lesstimate minimize functions of the form $$g(\pmb\theta) = f(\pmb\theta) + p(\pmb\theta)$$ where $f(\pmb\theta)$ is (twice) continously differentiable with respect to $\theta$ and $p(\pmb\theta)$ is a non-differentiable penalty function (e.g., lasso or scad). To use lesstimate for your project, you will need two functions. First, a function that computes $f(\pmb\theta)$, the value of your un- regularized objective function. Second, a function that computes $\triangledown_{\pmb\theta} f(\pmb\theta)$, the gradient vector of your un-regularized objective function with respect to the parameters $\pmb\theta$. We also assume that these functions use armadillo. If you don't use armadillo, you may have to write a translation layer. The optimizer interface outlined in the following is adapted from the ensmallen library (Curtin et al.; 2021).

Step 1: Including the necessary headers

First, let's include the necessary headers:

#include <RcppArmadillo.h>

// [[Rcpp :: depends ( RcppArmadillo )]]

#include <armadillo>

Step 2: Implement the fit and gradient functions:

Let's assume that you want to estimate a linear regression model. In this case, the fit and gradient function could look as follows:

double sumSquaredError(

arma::colvec b, // the parameter vector

arma::colvec y, // the dependent variable

arma::mat X // the design matrix

)

{

// compute the sum of squared errors:

arma::mat sse = arma::trans(y - X * b) * (y - X * b);

// other packages, such as glmnet, scale the sse with

// 1/(2*N), where N is the sample size. We will do that here as well

sse *= 1.0 / (2.0 * y.n_elem);

// note: We must return a double, but the sse is a matrix

// To get a double, just return the single value that is in

// this matrix:

return (sse(0, 0));

}

arma::rowvec sumSquaredErrorGradients(

arma::colvec b, // the parameter vector

arma::colvec y, // the dependent variable

arma::mat X // the design matrix

)

{

// note: we want to return our gradients as row-vector; therefore,

// we have to transpose the resulting column-vector:

arma::rowvec gradients = arma::trans(-2.0 * X.t() * y + 2.0 * X.t() * X * b);

// other packages, such as glmnet, scale the sse with

// 1/(2*N), where N is the sample size. We will do that here as well

gradients *= (.5 / y.n_rows);

return (gradients);

}

With these two functions, we are ready to go. If you want to use the glmnet optimizer, you may want to also implement a function that computes the Hessian. It can be beneficial to provide a good starting point for the bfgs updates using this Hessian.

Step 3: Creating a model object

lesstimate assumes that you pass a model-object to the optimizers. This model

object ist implemented in the less::model-class.

Therefore, we have to create a custom class that inherits from less::model and

implements our linear regression using the functions defined above.

Make sure to follow the install instructions for R first to make this work:

#include "lessSEM.h"

We recommend setting up lesstimate with CMake. You will find an example here.

#include <lesstimate.h>

// IMPORTANT: The library is called lesstimate, but

// because it was initially a sub-folder of lessSEM, there

// are two namespaces that are identical: less and lessSEM.

class linearRegressionModel : public less::model

{

public:

// the less::model class has two methods: "fit" and "gradients".

// Both of these methods must follow a fairly strict framework.

// First: They must receive exactly two arguments:

// 1) an arma::rowvec with current parameter values

// 2) an Rcpp::StringVector with current parameter labels

// (NOTE: the lessSEM package currently does not make use of these

// labels. This is just for future use. If you don't want to use

// the labels, just pass any less::stringVector you want).

// if you are using R, a less::stringVector is just an

// Rcpp::StringVector. Otherwise it is a custom vector. that can

// be created with less::stringVector myVector(numberofParameters).

// Second:

// 1) fit must return a double (e.g., the -2-log-likelihood)

// 2) gradients must return an arma::rowvec with the gradients. It is

// important that the gradients are returned in the same order as the

// parameters (i.e., don't shuffle your gradients, lessSEM will

// assume that the first value in gradients corresponds to the

// derivative with respect to the first parameter passed to

// the function).

double fit(arma::rowvec b, less::stringVector labels) override

{

// NOTE: In sumSquaredError we assumed that b was a column-vector. We

// have to transpose b to make things work

return (sumSquaredError(b.t(), y, X));

}

arma::rowvec gradients(arma::rowvec b, less::stringVector labels) override

{

// NOTE: In sumSquaredErrorGradients we assumed that b was a column-vector. We

// have to transpose b to make things work

return (sumSquaredErrorGradients(b.t(), y, X));

}

// IMPORTANT: Note that we used some arguments above which we did not pass to

// the functions: y, and X. Without these arguments, we cannot use our

// sumSquaredError and sumSquaredErrorGradients function! To make these

// accessible to our functions, we have to define them:

const arma::colvec y;

const arma::mat X;

// finally, we create a constructor for our class

linearRegressionModel(arma::colvec y_, arma::mat X_) : y(y_), X(X_){};

};

Instances of linearRegressionModel can be passed to the glmnet or ista optimizers.

Step 4: Interfacing to the optimizers

Ther are two interfaces you can use:

- A specialized interface, where the model is penalized only using one specific penalty function. This requires more work, but is typically a bit faster than using the second approach.

- A simplified interface that allows you to use any of the penalty functions (and also mix them)

We will use the simplified interface in the following. To this end, we will first create a new instance of our linearRegressionModel:

arma::mat X = {{1.00, -0.70, -0.86},

{1.00, -1.20, -2.10},

{1.00, -0.15, 1.13},

{1.00, -0.50, -1.50},

{1.00, 0.83, 0.44},

{1.00, -1.52, -0.72},

{1.00, 1.40, -1.30},

{1.00, -0.60, -0.59},

{1.00, -1.10, 2.00},

{1.00, -0.96, -0.20}};

arma::colvec y = {{ 0.56},

{-0.32},

{ 0.01},

{-0.09},

{ 0.18},

{-0.11},

{ 0.62},

{ 0.72},

{ 0.52},

{ 0.12}};

linearRegressionModel linReg(y, X);

Next, we create a vector with starting values using armadillo. This vector must be of length of the number of parameters in the model. In our case, these are three: the intercept and two predictors.

arma::rowvec startingValues(3);

startingValues.fill(0.0);

less::stringVector:

When using R, less::stringVector is identical to Rcpp::StringVector.

Rcpp::StringVector parameterLabels(3);

parameterLabels[0] = "b0";

parameterLabels[1] = "b1";

parameterLabels[2] = "b2";

std::vector<std::string> labels {"b0", "b1", "b2"};

less::stringVector parameterLabels(labels);

Now we have to specify the values for our tuning parameters. These depend on the penalty we want to use:

Note that some penalty functions only have $\lambda$ as tuning parameter, while others have $\lambda$ and $\theta$. The interface used below does not support elastic net penalties; that is, $\alpha$ is not used. Furthermore, the adaptive lasso requires setting up the weights manually by specifying parameter-specific $\lambda$-values. We now specify for each parameter, which penalty we want to use and what values the tuning parameter should have for this parameter. If a tuning parameter is not used by the respective penalty, just set it to 0 or any other value:

// penalty: We don't penalize the intercept b0, but we penalize

// b1 and b2 with lasso:

std::vector<std::string> penalty{"none", "lasso", "lasso"};

// tuning parameter lambda:

arma::rowvec lambda = {{0.0, 0.2, 0.2}};

// theta is not used by the lasso penalty:

arma::rowvec theta = {{0.0, 0.0, 0.0}};

// penalty: We don't penalize the intercept b0, but we penalize

// b1 with lasso and b2 with scad:

std::vector<std::string> penalty{"none", "lasso", "scad"};

// tuning parameter lambda:

arma::rowvec lambda = {{0.0, 0.2, 0.1}};

// theta is not used by the lasso penalty:

arma::rowvec theta = {{0.0, 0.0, 3.6}};

Note that the penalty used for each parameter is specified in the std::vector<std::string> vector penalty.

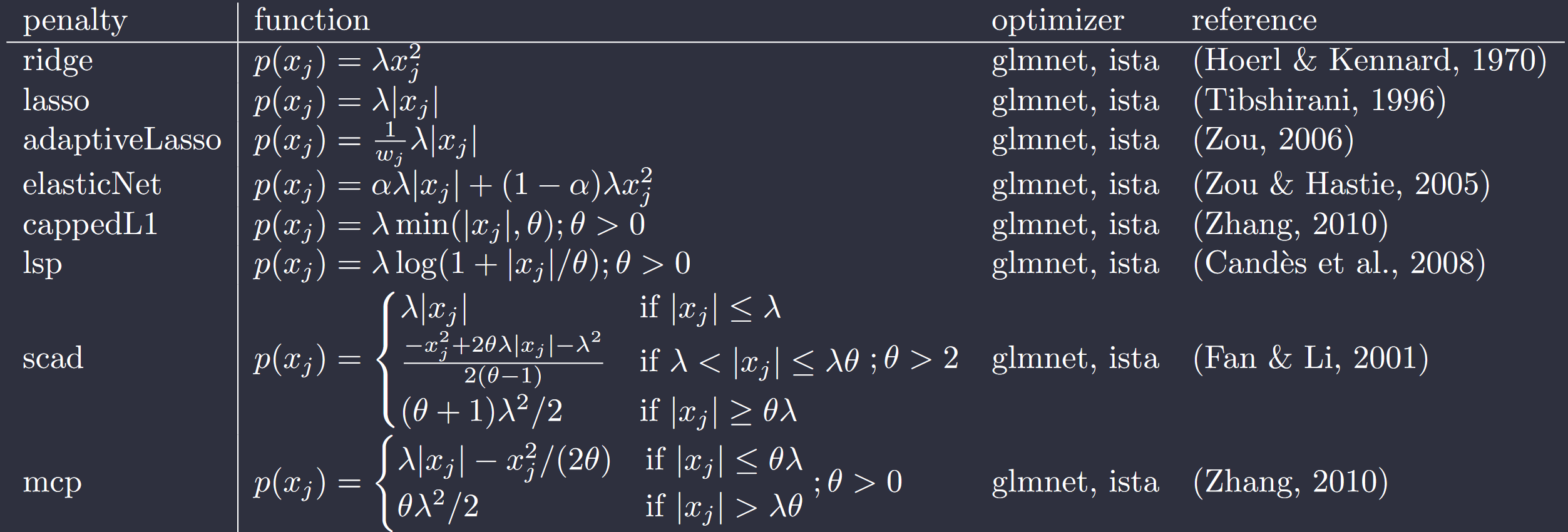

Currently, any of the following penalty labels is supported: "none" (no penalty), "cappedL1", "lasso",

"lsp", "mcp", and "scad".

Having specified the penalty and the tuning values, we can now use the optimizers:

To use glmnet successfully, you should also provide an initial Hessian as this can improve the optimization considerably. For simplicity, we won't do this here.

less::fitResults fitResult_ = less::fitGlmnet(

linReg,

startingValues,

parameterLabels,

penalty,

lambda,

theta//,

// initialHessian, // optional, but can be very useful

// controlOptimizer, // optional: change the settings of the optimizer.

// verbose // set to >0 to get additional information on the optimization

);

less::fitResults fitResult_ = less::fitIsta(

linReg,

startingValues,

parameterLabels,

penalty,

lambda,

theta//,

// controlOptimizer, // optional: change the settings of the optimizer

// verbose // set to >0 to get additional information on the optimization

);

In the fitResults_ object, you will find:

- fit: the final fit value (regularized fit)

- fits: a vector with all fits at the outer iteration

- convergence: was the outer breaking condition met?

- parameterValues: final parameter values (of class

arma::rowvec) - Hessian: final Hessian approximation in case of glmnet (Note: this is a bfgs approximated Hessian). Returning this Hessian is useful because it can be used as input for the next optimization if glmnet is used with multiple tuning parameter settings (e.g., $\lambda \in {0, .1, .2, ..., 1}$.

Optimizer settings

The default settings of the optimizers may not work for your use case. Adapting these settings can therefore be crucial for a

succesful optimization. In the fitGlmnet and fitIsta functions above, the optimizer settings are adapted using the controlOptimizer

argument. Depending on the optimizer used, different settings can be adapted.

The glmnet optimizer has the following additional settings:

initialHessian: anarma::matwith the initial Hessian matrix fo the optimizer. In case of the simplified interface, this argument should not be used. Instead, pass the initial Hessian as shown abovestepSize: adoublespecifying the initial stepSize of the outer iteration ($\theta_{k+1} = \theta_k + \text{stepSize} * \text{stepDirection}$)sigma: adoublethat is only relevant when lineSearch = 'GLMNET'. Controls the sigma parameter in Yuan, G.-X., Ho, C.-H., & Lin, C.-J. (2012). An improved GLMNET for l1-regularized logistic regression. The Journal of Machine Learning Research, 13, 1999–2030. https://doi.org/10.1145/2020408.2020421.gamma: adoublecontroling the gamma parameter in Yuan, G.-X., Ho, C.-H., & Lin, C.-J. (2012). An improved GLMNET for l1-regularized logistic regression. The Journal of Machine Learning Research, 13, 1999–2030. https://doi.org/10.1145/2020408.2020421. Defaults to 0.maxIterOut: anintspecifying the maximal number of outer iterationsmaxIterIn: anintspecifying the maximal number of inner iterationsmaxIterLine: anintspecifying the maximal number of iterations for the line search procedurebreakOuter: adoublespecyfing the stopping criterion for outer iterationsbreakInner: adoublespecyfing the stopping criterion for inner iterationsconvergenceCriterion: aconvergenceCriteriaGlmnetspecifying which convergence criterion should be used for the outer iterations. Possible areless::GLMNET,less::fitChange, andless::gradients.verbose: anint, where 0 prints no additional information, > 0 prints GLMNET iterations

// First, create a new instance of class controlGLMNET:

less::controlGLMNET controlOptimizer = less::controlGlmnetDefault();

// Next, adapt the settings:

controlOptimizer.maxIterOut = 1000;

// pass the argument to the fitGlmnet function:

less::fitResults fitResult_ = less::fitGlmnet(

linReg,

startingValues,

parameterLabels,

penalty,

lambda,

theta,

// sets Hessian to identity; a better Hessian will help!

arma::mat(1, 1, arma::fill::ones), // initial Hessian

controlOptimizer//,

// verbose // set to >0 to get additional information on the optimization

);

The ista optimizer has the following additional settings:

L0: adoublecontroling the step size used in the first iterationeta: adoublecontroling by how much the step size changes in inner iterations with $(\eta^i)*L$, where $i$ is the inner iterationaccelerate: abool; if the extrapolation parameter is used to accelerate ista (see, e.g., Parikh, N., & Boyd, S. (2013). Proximal Algorithms. Foundations and Trends in Optimization, 1(3), 123–231., p. 152)maxIterOut: anintspecifying the maximal number of outer iterationsmaxIterIn: anintspecifying the maximal number of inner iterationsbreakOuter: adoublespecyfing the stopping criterion for outer iterationsbreakInner: adoublespecyfing the stopping criterion for inner iterationsconvCritInner: aconvCritInnerIstathat specifies the inner breaking condition. Can be set toless::istaCrit(see Beck & Teboulle (2009); Remark 3.1 on p. 191 (ISTA with backtracking)) orless::gistCrit(see Gong et al., 2013; Equation 3)sigma: adoublein (0,1) that is used by the gist convergence criterion. Larger sigma enforce larger improvement in fitstepSizeIn: astepSizeInheritancethat specifies how step sizes should be carried forward from iteration to iteration.less::initial: resets the step size to L0 in each iteration,less::istaStepInheritance: takes the previous step size as initial value for the next iteration,less::barzilaiBorwein: uses the Barzilai-Borwein procedure,less::stochasticBarzilaiBorwein: uses the Barzilai-Borwein procedure, but sometimes resets the step size; this can help when the optimizer is caught in a bad spot.sampleSize: anintthat can be used to scale the fitting function down if the fitting function depends on the sample sizeverbose: anint, where 0 prints no additional information, > 0 prints GLMNET iterations

// First, create a new instance of class controlIsta:

less::controlIsta controlOptimizer = less::controlIstaDefault();

// Next, adapt the settings:

controlOptimizer.maxIterOut = 1000;

// pass the argument to the fitIsta function:

less::fitResults fitResult_ = less::fitIsta(

linReg,

startingValues,

parameterLabels,

penalty,

lambda,

theta,

controlOptimizer//,

// verbose // set to >0 to get additional information on the optimization

);

Specialized interfaces

If you are only interested in one specific penalty function (e.g., lasso), it can be beneficial to use the specialized interfaces provided by lesstimate. These can be faster because lesstimate no longer has to check which penalty is used for which parameter. That said, the specialized interface takes some more time to set up and is less flexible than the simplified interface used above.

To use the specialized interface, we have to define the penalties we want to use. In general, the specialized interface allows for specifying two penalties for each parameter: a smooth (i.e., differentiable) penalty (currently only ridge is supported) and a non-smooth (i.e., non-differentiable) penalty (any of the penalties mentioned above). We will use the elastic net below as this penalty combines a ridge and a lasso penalty.

// Specify the penalties we want to use:

less::penaltyLASSOGlmnet lasso;

less::penaltyRidgeGlmnet ridge;

// Note that we used the glmnet variants of lasso and ridge. The reason

// for this is that the glmnet implementation allows for parameter-specific

// lambda and alpha values while the current ista implementation does not.

// These penalties take tuning parameters of class tuningParametersEnetGlmnet

less::tuningParametersEnetGlmnet tp;

// We have to specify alpha and lambda. Here, different values can

// be specified for each parameter:

tp.lambda = arma::rowvec(startingValues.n_elem);

tp.lambda.fill(0.2);

tp.alpha = arma::rowvec(startingValues.n_elem);

tp.alpha.fill(0.3);

// Finally, there is also the weights. The weights vector indicates, which

// of the parameters is regularized (weight = 1) and which is unregularized

// (weight =0). It also allows for adaptive lasso weights (e.g., weight =.0123).

// weights must be an arma::rowvec of the same length as our parameter vector.

arma::rowvec weights(startingValues.n_elem);

weights.fill(1.0); // we want to regularize all parameters

weights.at(0) = 0.0; // except for the first one, which is our intercept.

tp.weights = weights;

// to optimize this model, we have to pass it to

// the glmnet function:

less::fitResults lmFit = less::glmnet(

linReg, // the first argument is our model

startingValues, // arma::rowvec with starting values

parameterLabels, // less::stringVector with labels

lasso, // non-smooth penalty

ridge, // smooth penalty

tp//, // tuning parameters

//controlOptimizer // optional fine-tuning (see above)

);

// The elastic net is a combination of a ridge penalty and

// a lasso penalty.

// NOTE: HERE COMES THE BIGGEST DIFFERENCE BETWEEN GLMNET AND ISTA:

// 1) ISTA ALSO REQUIRES THE DEFINITION OF A PROXIMAL OPERATOR. THESE

// ARE CALLED proximalOperatorZZZ IN lessSEM (e.g., proximalOperatorLasso

// for lasso).

// 2) THE SMOOTH PENALTY (RIDGE) AND THE LASSO PENALTY MUST HAVE SEPARATE

// TUNING PARMAMETERS.

less::proximalOperatorLasso proxOp; // HERE, WE DEFINE THE PROXIMAL OPERATOR

less::penaltyLASSO lasso;

less::penaltyRidge ridge;

// BOTH, LASSO AND RIDGE take tuning parameters of class tuningParametersEnet

less::tuningParametersEnet tpLasso;

less::tuningParametersEnet tpRidge;

// We have to specify alpha and lambda. Here, the same value is used

// for each parameter:

tpLasso.alpha = .3;

tpLasso.lambda = .2;

tpRidge.alpha = .3;

tpRidge.lambda = .2;

// A weights vector indicates, which

// of the parameters is regularized (weight = 1) and which is unregularized

// (weight =0). It also allows for adaptive lasso weights (e.g., weight =.0123).

// weights must be an arma::rowvec of the same length as our parameter vector.

arma::rowvec weights(startingValues.n_elem);

weights.fill(1.0); // we want to regularize all parameters

weights.at(0) = 0.0; // except for the first one, which is our intercept.

tpLasso.weights = weights;

tpRidge.weights = weights;

// to optimize this model, we have to pass it to the ista function:

less::fitResults lmFit = less::ista(

linReg, // the first argument is our model

startingValues, // arma::rowvec with starting values

parameterLabels, // less::stringVector with labels

proxOp, // proximal opertator

lasso, // our lasso penalty

ridge, // our ridge penalty

tpLasso, // our tuning parameter FOR THE LASSO PENALTY

tpRidge//, // our tuning parameter FOR THE RIDGE PENALTY

//controlOptimizer // optional fine-tuning (see above)

);

References

- Sanderson C, Curtin R (2016). Armadillo: a template-based C++ library for linear algebra. Journal of Open Source Software, 1 (2), pp. 26.

- Eddelbuettel D, François R (2011). “Rcpp: Seamless R and C++ Integration.” Journal of Statistical Software, 40(8), 1–18. doi:10.18637/jss.v040.i08.

- Eddelbuettel D, Sanderson C (2014). “RcppArmadillo: Accelerating R with high-performance C++ linear algebra.” Computational Statistics and Data Analysis, 71, 1054–1063. doi:10.1016/j.csda.2013.02.005.

- Curtin R R, Edel M, Prabhu R G, Basak S, Lou Z, Sanderson C (2021). The ensmallen library for flexible numerical optimization. Journal of Machine Learning Research, 22 (166).